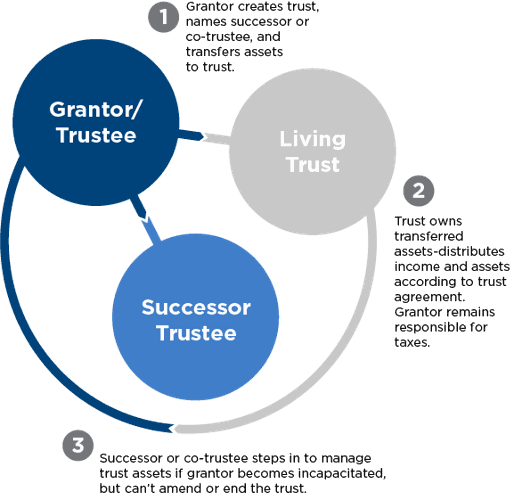

The basics of trusts are easy to understand. Trusts are legal entities that allow one party to manage assets for the benefit of another. They involve three key roles: the grantor who establishes the trust, the trustee who manages the trust, and the beneficiary who receives the benefits. You can create a trust by executing a legal document called a trust agreement, which lists the beneficiary and the trustee, and explains the benefits the beneficiary will receive and the trustee’s duties. This document is usually part of the estate planning process.

You can fund your trust with cash, stocks, bonds, insurance policies, real estate, artwork, vacation homes, and many other assets. What you choose will depend on your goals for the trust. For example, bonds are ideal for income generation, whereas life insurance policies are useful for creating funds to cover estate taxes or to support your family after your death.

There are many advantages to creating a trust. A trust can reduce estate taxes, protect assets from potential creditors, bypass the lengthy and costly probate process of settling a deceased person’s estate, and preserve assets for minors in case of your death. Trusts can also create a pool of money to be managed professionally, support the grantor if incapacitated, shift tax burdens to lower-income beneficiaries, and support charitable causes.

Potential disadvantages include the cost of creating and maintaining a trust, such as trustee fees, professional fees, and filing fees. Depending on the type of trust, you may give up some control over certain assets, and income generated by trust assets and not distributed to trust beneficiaries may be taxed at a higher income tax rate than your individual rate.

The most basic types of trusts are revocable (living) and irrevocable trusts. A living trust is created when you’re alive and can continue after your death. You can direct the trustee to hold trust property until the beneficiary reaches a certain age or gets married. Living trusts have some drawbacks. Property in a living trust is generally not protected from creditors, and you cannot avoid estate taxes using a living trust.

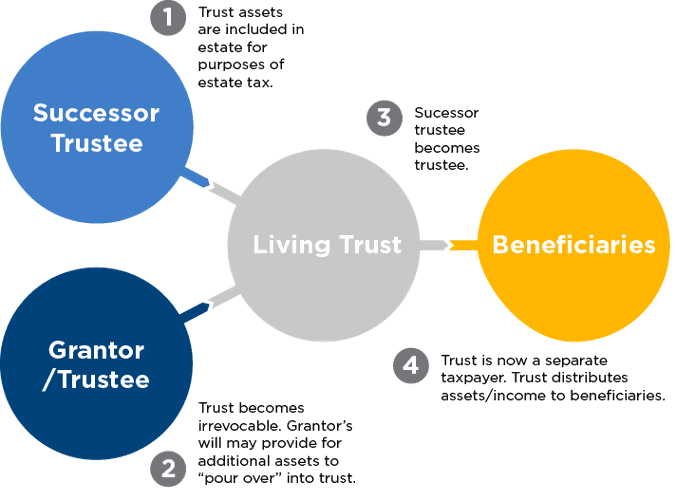

An irrevocable trust is not easily changed or revoked. For this type of trust, you usually cannot change beneficiaries or change the terms. Irrevocable trusts are frequently used to help reduce potential estate taxes. The transfer may be subject to gift tax at the time when a property is transferred into the trust, but the property, plus any future appreciation, is usually removed from your gross estate. Additionally, property transferred through an irrevocable trust will avoid probate and may be protected from future creditors.

For help deciding which type of trust might best fit your needs and goals, contact CAPTRUST.

To read the full CAPTRUST article, click here.

{kind=link}

{kind=link}